April 6, 2026

What Every Homeowner Should Know Before Filing a Claim

Colorado's hail season is one of the most active in the entire country. If your home has been through a recent storm, you may be asking yourself: Is this covered by my insurance? Do I need to call my insurance company? What if I wait a little longer?

These are smart questions — and knowing the answers ahead of time puts you in control of a process that can feel confusing and overwhelming. This post walks you through what Colorado homeowners insurance typically covers, what deadlines you need to know, and how to make a wise, well-informed decision for your home.

What Colorado Homeowners Insurance Typically Covers

Most standard homeowners insurance policies cover roof damage that is sudden and caused by a specific event — like a hailstorm, windstorm, or falling tree. This is called a "covered peril."

What is generally NOT covered:

• Normal wear and tear over time

• Gradual deterioration or aging

• Damage from a lack of maintenance

In plain terms: if your roof was damaged by a storm, there's a good chance it's covered. If it's just old and worn out, that's a different conversation.

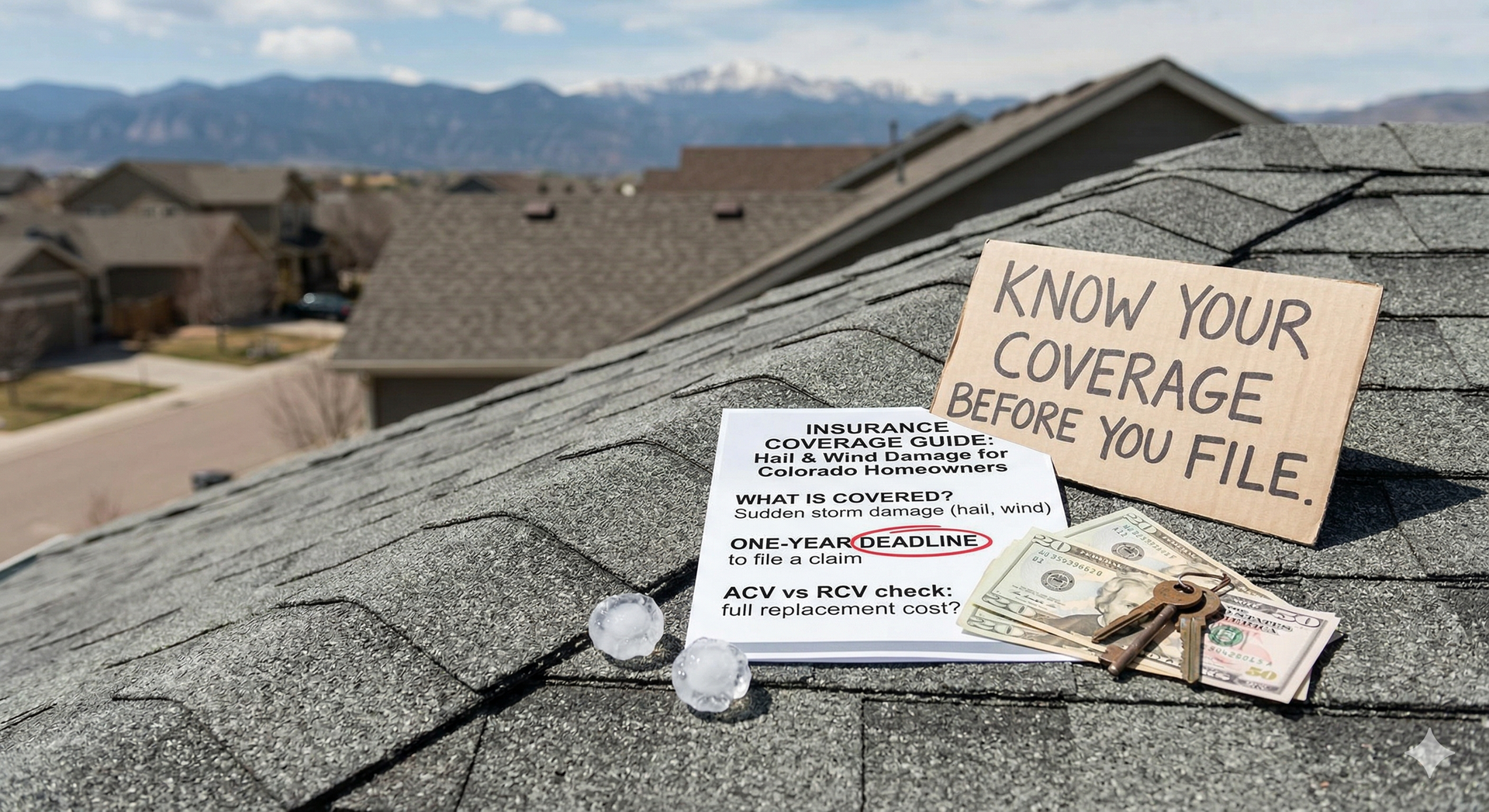

One important thing to check: whether your policy pays out based on Actual Cash Value (ACV) or Replacement Cost Value (RCV). ACV policies subtract depreciation — meaning older roofs may receive a smaller payout. RCV policies pay the full cost to replace the roof with a comparable new one. This is worth a quick call to your agent to clarify.

Pro tip: Ask your agent, "Do I have ACV or RCV coverage on my roof?" The answer directly affects how much money you could receive after a claim.

The One-Year Deadline Most Homeowners Don't Know About

This may be the most important piece of information in this entire post.

In Colorado, homeowners generally have one year from the date of a storm event to file a hail or wind damage claim with their insurance company. This is not a rule that most people know — and it catches many homeowners off guard.

Here's what often happens: A storm moves through in May. The roof looks okay from the ground. Life gets busy. Then in January, a homeowner notices a stain on their ceiling. By the time they call a contractor and get an inspection, they've missed the window to file.

Waiting doesn't make the damage disappear — it often makes it worse. Hail damage can compromise shingles in ways that aren't visible to the eye but accelerate wear, allow moisture in, and lead to bigger problems down the road.

Important: The one-year clock starts on the date of the storm — not the date you discover the damage. If a significant storm hit your area in the last 12 months, it's worth getting a professional inspection sooner rather than later.

What Insurance Adjusters Look For

When an insurance adjuster comes to inspect your roof, they're looking for specific signs of storm damage. Knowing what they look for helps you understand whether your damage is likely to be approved or denied.

Common signs of hail damage on a roof:

• Granule loss — small granules from asphalt shingles collecting in your gutters or around your downspouts

• Dented metal — vents, flashing, gutters, and downspouts are soft metal and show impact marks clearly

• Bruised shingles — hail strikes create a soft spot beneath the surface of the shingle that isn't always visible without a trained eye

• Cracked or split shingles — especially common with older roofs or larger hail

One advantage of working with a roofing contractor before your adjuster arrives: a professional inspection — including drone technology — can document damage thoroughly and give you an accurate picture of what's there. This helps you go into the adjuster visit informed.

At UB Code Roofing, we use FAA-certified drone inspections to safely and accurately document roof damage. Our detailed damage reports help homeowners understand exactly what they have before talking to their insurance company.

Smart Questions to Ask Your Insurance Company

Before you decide whether or not to file a claim, it's worth calling your insurance agent and asking a few direct questions. Here are the ones that matter most:

• "What is my current roof deductible?" — Some policies have a separate hail or wind deductible that is higher than your standard deductible.

• "Do I have ACV or RCV coverage on my roof?" — This determines your payout amount.

• "Will my premium increase if I file a hail damage claim?" — In Colorado, insurers are generally not allowed to non-renew your policy solely for filing a weather-related claim, but premiums can still be affected.

• "Was there a named storm event in my area on [date]?" — Insurers track storm events, and having the date confirms your claim is tied to a specific storm.

These are not aggressive or confrontational questions. They're the same questions a smart, informed homeowner should ask before making any financial decision.

When It Might NOT Make Sense to File a Claim

Here's something you may not expect a roofing company to say: filing an insurance claim isn't always the right move.

If the damage to your roof is minimal — a few shingles, a small section — and the cost to repair it is close to or less than your deductible, filing a claim may not be worth it. You'd be paying out of pocket up to your deductible anyway, and the claim could affect your premium history.

A good contractor will give you an honest assessment and help you weigh the numbers. The goal is to help you make the best decision for your home and your budget — not just to generate a job.

Honest advice is the foundation of a good contractor relationship. At UB Code Roofing, we'll tell you what we see and help you understand your options — without pressure.

Frequently Asked Questions

Does homeowners insurance always cover hail damage to a roof in Colorado?

Not always. Coverage depends on your policy type, the age and condition of your roof, and how the damage occurred. Most standard policies cover sudden storm damage, but the payout amount varies based on ACV vs. RCV coverage.

What if my insurance claim for roof damage is denied?

If your claim is denied, you have options. You can request a re-inspection, provide additional documentation, or work with a public adjuster to appeal the decision. A detailed inspection report from your contractor can support your case.

How long does a hail damage roof claim take in Colorado?

Most claims move fairly quickly once filed — often within 2 to 4 weeks from inspection to approval. The overall project timeline depends on scheduling, material availability, and permit processing in your area.

Can I file a roof insurance claim for storm damage from last year?

In Colorado, you generally have one year from the date of the storm to file. If you're within that window, it's worth getting an inspection to assess whether you have a valid claim.

Not sure if your roof sustained storm damage? A free inspection — including drone documentation — gives you the facts you need to make a confident decision. Call UB Code Roofing at 303-225-4620 | ubcoderoofing.com